6 High Net Worth Tax Planning Strategies

- April 23, 2026

- Posted by: CKH Group

- Categories: Financial Tips, Tax tips

High Net Worth Tax Planning Strategies: A Guide for $1 Million+ Portfolios

Managing a portfolio worth $1 million or more comes with financial rewards and a significantly more complex tax landscape. At these wealth levels, traditional tax filing approaches simply aren’t enough. A proactive, year-round tax strategy can make a six-figure difference in your annual liability and long-term wealth accumulation.

This guide walks through six high net worth tax planning strategies available to investors in 2026, backed by current IRS rules and updated for the most recent tax legislation, such as the One Big Beautiful Bill Act (OBBBA).

What is Your Tax Exposure at $1 Million+?

Before exploring strategies, it’s important to recognize what tax exposure higher-income investors are actually facing:

Top marginal income tax rate: The top marginal income tax rate reaches 37% in 2026, meaning that income above $640,600 for single filers or $768,700 for married couples is taxed at this highest bracket. This is not the entirety of your income, but each additional dollar earned beyond those thresholds.

Long-term capital gains tax: Investment income is taxed differently. Long-term capital gains, which apply to profits from selling assets like stocks or real estate held for more than a year, are taxed at rates up to 20%. On top of that, high earners are also subject to the 3.8% Net Investment Income Tax (NIIT) under IRC §1411, an additional surtax applied once AGI exceeds $200,000 (single) or $250,000 (married)

Estate tax: Estate taxes add another layer of complexity. While the current federal exemption sits at approximately $13.99 million per individual, that exemption could change in future years.

The combined effect of these taxes means that many high-income earners see total tax exposure approach or exceed one-third of their income. That’s why strategic planning becomes essential.

Tax Planning Strategies for High Net Worth Individuals

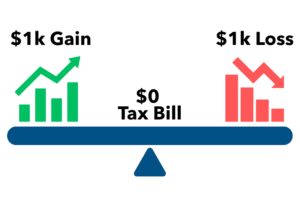

1. Tax-Loss Harvesting: Turning Losses into Long-Term Gains

Tax-loss harvesting involves intentionally selling underperforming investments to realize losses that offset capital gains elsewhere in your portfolio. For example, if you made 50k in profit on one investment but lost 20k on another, you can use that loss to reduce the taxable gain to 30k.

Research from Vanguard’s Investment Strategy Group suggests tax-loss harvesting can add between 0.5% and 1.5% annually to after-tax returns in volatile market conditions. At $1 million+ portfolios, even a 1% improvement on $1.5 million in taxable holdings represents $15,000 saved annually, which compounds significantly over time.

Be mindful of the IRS wash-sale rule (IRC §1091), which disallows the deduction if you repurchase a “substantially identical” security within 30 days before or after the sale. In other words, you can’t sell a stock just to claim a loss and then immediately buy it back. However, as mentioned in our article “5 Cyrpto Tax Tips” certain investments, such as crypto, might not fall under this IRS wash-sale rule (as of April 2026).

2. Strategic Roth Conversions and Backdoor Roth Contributions

Roth IRAs are one of the most powerful long-term tax planning tools available because they allow investments to grow completely tax-free, with no required minimum distributions later in life for the original account owner.

High-income earners are phased out of direct Roth IRA contributions ($236,000 AGI for married filers in 2026), but the backdoor Roth conversion remains a legal workaround that provides an alternative path. This involves making a non-deductible contribution to a traditional IRA (where income limits do not apply), and then immediately converting it to a Roth IRA. Per IRS guidance, this is permissible as long as the pro-rata rule is carefully managed.

Roth accounts grow tax-free and carry no required minimum distributions (RMDs) for original account holders, making them especially powerful for high-net-worth individuals with multi-generational wealth goals. Strategic conversions during lower-income years (partial retirement, business sale transition periods) can lock in tax-free growth for decades.

3. Maximize Charitable Giving with Donor-Advised Funds

A Donor-Advised Fund (DAF) functions as a centralized charitable account that allows you to contribute assets, receive an immediate tax deduction, and then distribute those funds to charities over time. This flexibility is particularly valuable for high-net-worth individuals who want to separate the timing of their tax deduction from the timing of their charitable giving.

Using a DAF allows you to make a charitable contribution, receive an immediate tax deduction, and distribute the funds to charities over time. According to Fidelity Charitable’s 2024 Giving Report, the average DAF contribution was over $35,000.

One of the most effective uses of a DAF is contributing highly appreciated securities rather than donating cash; investments like stocks or assets that have significantly increased in value since you purchased them. By donating the asset directly instead of selling it first, you avoid paying capital gains tax on the increase in value while still receiving a charitable deduction for the full fair market value.

This strategy also pairs well with “bunching” contributions- making multiple years of charitable contributions in a single year to exceed the standard deduction threshold and maximize tax efficiency.

In our article on Charitable Giving in 2025 and 2026 under OBBBA, Donor-Advised Funds were a particularly useful strategy to make charitable contributions before the new AGI floor restrictions were put in place under OBBBA.

4. Qualified Opportunity Zone (QOZ) Investments

Qualified Opportunity Zones are designated geographic areas identified by the federal government to encourage economic development through private investment. These zones are typically located in economically distressed communities, and in exchange for investing in them, taxpayers can access a unique set of tax incentives.

Created under the 2017 Tax Cuts and Jobs Act and available through Qualified Opportunity Funds, QOZ investments offer three potential tax benefits:

Created under the 2017 Tax Cuts and Jobs Act and available through Qualified Opportunity Funds, QOZ investments offer three potential tax benefits:

-

- Deferral of Capital Gains- The primary benefit is the ability to defer capital gains. Investors can reinvest gains from the sale of assets such as stocks, real estate, or business interests into a QOZ fund and delay paying taxes on those gains until the fund is sold or December 31, 2026. A follow up to the QOZ fund program was released with OBBBA last year.

-

- Potential Step-Up in Basis after Holding Periods – Your “basis” is the value the IRS uses to calculate taxable gain. A step-up increases that baseline, which reduces the portion of the investment that is ultimately taxed. While the exact benefit depends on holding period rules and current legislation, the intent is to reward longer-term investment in these areas.

-

- Permanent exclusion of gains if held 10 years – Long-term holding creates the most significant advantage. If the investment is held for at least 10 years, any appreciation on the QOZ investment itself can be excluded from taxation entirely, making it both a tax planning and long-term growth strategy.

The IRS maintains a list of designated Qualified Opportunity Zones.

5. Estate Planning: Don’t Wait for the Exemption Cliff

The current federal estate tax exemption of ~$13.99 million per person ($27.98 million per couple) is historically high, which presents a window of opportunity for wealth planning. Future legislative changes remain a real possibility, so high-net-worth individuals should consider structures that lock in current exemptions, such as:

- Grantor Retained Annuity Trusts (GRATs): Transfer asset appreciation out of your estate with minimal gift tax exposure

- Spousal Lifetime Access Trusts (SLATs): Utilize the estate tax exemption while retaining indirect access to assets

- Annual gifting: The 2026 annual gift tax exclusion is $19,000 per recipient. A couple can give $38,000 per person, per year, completely tax-free

- Stepped-up basis planning: Assets held until death receive a step-up in cost basis, potentially eliminating lifetime capital gains on appreciated property

6. Business Structure and Pass-Through Optimization

For business owners, tax planning extends beyond investments into how the business itself is structured.

Pass-through entities such as S-Corporations and LLCs allow business income to flow directly to the owner’s personal tax return rather than being taxed at the corporate level. Under current law, eligible businesses may qualify for the Qualified Business Income (QBI) deduction, which allows up to 20% of that income to be deducted.

Additional strategies such as setting reasonable compensation in an S-Corp structure, contributing to retirement plans like SEP-IRAs or defined benefit plans, and timing income recognition can further reduce overall tax liability.

Working with a CPA Who Understands High Net Worth Complexity

The strategies above are powerful individually, but the greatest results come from integrating them into a cohesive, forward-looking plan that accounts for your full financial picture. Tax law changes, investment activity, charitable goals, and estate planning objectives all interact in ways that require coordinated, expert guidance. Even if you have a keen understanding of your taxes and tax filing compliance, a CPA can help you make the most of your tax strategies.

At CKH Group, our tax professionals specialize in high-net-worth tax planning across income tax, capital gains, estate planning, and international considerations. Contact Us to discuss your portfolio and identify opportunities.

The above article only intends to provide general financial information and is based on open-source facts, it is not designed to provide specific advice or recommendations for any individual. It does not give personalized tax, financial, or other business and professional advice. Before taking any form of action, you should consult a financial professional who understands your particular situation. CKH Group will not be held liable for any harm/errors/claims arising from the articles. Whilst every effort has been taken to ensure the accuracy of the contents, we will not be held accountable for any changes that are beyond our control.