5 Vacation Rental Tax Tips

- May 5, 2026

- Posted by: CKH Group

- Categories: Financial Tips, Tax tips

Vacation Rental Tax Tips: 5 Smart Strategies for Property Owners

With warmer weather and tax season behind us, summer travel plans are now on the horizon. If you own a vacation rental, that usually means more guests, more income… and more to keep track of on the tax side.

Vacation rentals can be a powerful source of income, but they also come with a unique set of tax rules that can be overlooked. Whether you’re renting out a beach house a few weeks a year or operating a full-time short-term rental, understanding how your property is classified and taxed is critical to avoiding surprises and maximizing deductions.

With increased IRS attention on short-term rental activity, expanded platform reporting requirements (such as Form 1099-K thresholds now fully in effect), and evolving local tax rules, staying informed is more important than ever.

Below are five essential vacation rental tax tips to help you stay compliant and optimize your tax position in 2026.

How Vacation Rentals Are Classified for Tax Purposes

Before diving into deductions and strategies, the most important step is understanding how your rental is classified for tax purposes. The IRS doesn’t simply label properties as “short-term” or “long-term” based on how you market them. It looks at usage, rental days, and personal use to determine how your property is taxed.

Getting this classification wrong can lead to missed deductions, unexpected tax bills, or compliance issues.

Short-Term Rentals (STRs)

Short-term rentals typically refer to properties rented for an average stay of 7 days or less (or sometimes 30 days or less, depending on context and local regulations). Income is generally reported on Schedule E and in some cases (if substantial services are provided), it may be reported on Schedule C.

STRs can qualify for unique tax advantages, including potential exceptions to passive activity loss rules. These are your typical listings on platforms like Airbnb or Vrbo.

Long-Term Rentals

Long-term rentals involve tenants staying for extended periods (generally 30 days or more) under a lease agreement. Income is almost always reported on Schedule E and subject to standard passive activity rules.

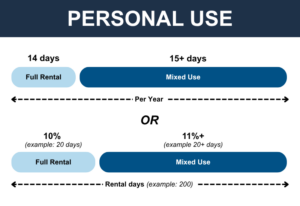

Mixed-Use vs Full Rental Properties

Mixed-Use vs Full Rental Properties

An important item to note is that the IRS also looks at personal use to determine eligibility. If personal use exceeds 14 days or 10% of rental days (whichever is greater), the classification changes to mixed-use property. This is important because mixed-use properties require you to split expenses between personal and rental use, and full rental properties allow broader deductions and potential loss treatment.

Vacation Rental Tax Tips

1. The Augusta Rule / 14-Day Rule

For a property to be considered a rental (short or long term), it must be rented more than 14 days in a year. But this brings up an interesting caveat- what if you rent your property less than 14 days in a year?

This is sometimes referred to as the Augusta rule, and allows for tax-free rental income if you do not exceed 14 days. This rule is often used strategically during high-demand events (think major sporting events or festivals) and was made popular by residents of Augusta, Georgia who wanted to rent their homes tax free for 14 days during the annual Masters Golf Tournament in the area.

However, there is a tradeoff. You cannot deduct rental expenses beyond property taxes and mortgage interest (as a personal residence) if you utilize the Augusta Rule. If you do exceed 14 days, it is classified as a rental and you must report the income.

Recently, business owners have been utilizing the Augusta rule as a tax-saving strategy of renting your home to your business (for legitimate business purposes such as meetings, trainings, or retreats) so that the business can deduct the rental cost while the homeowner excludes the income from personal taxes. However, it is important to note that this tax strategy requires legitimate business purpose (ordinary and necessary), documentation, and follows Fair Market Value (FMV)- otherwise you may be inviting IRS scrutiny.

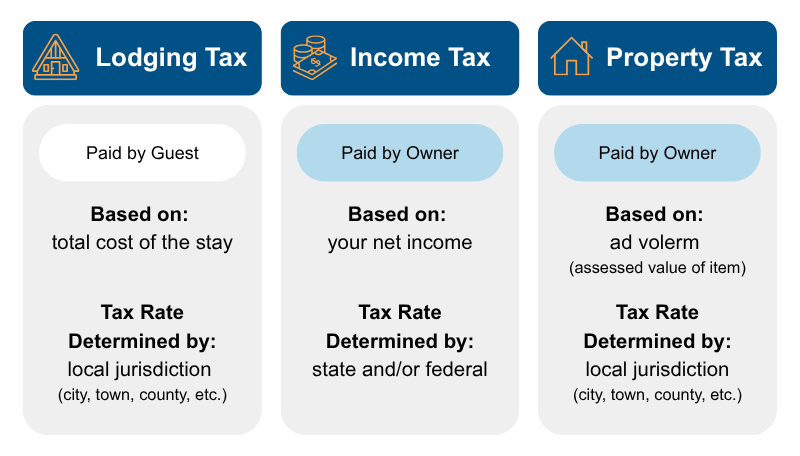

2. Lodging Taxes vs. Property Taxes vs. Income Taxes

Rental owners deal with three very different tax systems, and understanding them is important to being in compliance with your tax obligations throughout the year.

Lodging (Occupancy) Taxes

Lodging taxes are paid by the guest and include state, county, and city taxes (similar to hotel taxes). Platforms like Airbnb and Vrbo may collect and remit these automatically, but not always. This is important to keep in mind if you handle payments and bookings independent of platforms like this.

Even if a platform collects lodging tax, you are still responsible for ensuring compliance with local regulations. Many jurisdictions require separate registration or filings.

Income Taxes

Just like you would for standard W-2 income, income taxes are paid by you, the owner, and are based on your net rental income. This is reported on Schedule E (or Schedule C in some cases).

Property Taxes

Property tax is an ad valorem tax that is also paid by you, the owner. Ad valorem means ‘according to value’ and in the tax world that means it is a tax based on the assessed value of the item (rather than quantity or size). This is calculated by the local government where your property is located, and can vary by jurisdiction.

If you’re looking to purchase a property and want to save on property taxes, purchasing in areas with lower effective property tax rates is a strategy you can use.

3. Maximize Common Vacation Rental Deductions

If your property qualifies as a rental, you can deduct a wide range of ordinary and necessary expenses, including:

-

- Mortgage interest

- Property taxes

- Utilities (electric, water, internet)

- Cleaning and maintenance

- Property management fees

- Insurance

- Advertising and listing fees

- Supplies and furnishings

- Depreciation

Remember, if your property is classified as mixed-use, these expenses must be allocated between personal and rental use, so you cannot deduct 100% of them- instead you would deduct a percentage for rental use.

For example, if you rented 200 days out of the year and had 40 days of personal use, your rental use percentage would be 83.3% (200 divided by 240 total days). Then, 83.3% of eligible shared expenses would be deductible. Some expenses don’t need allocation if they are only related to rental activity (such as property management fees, listing costs, or cleaning fees between guest stays).

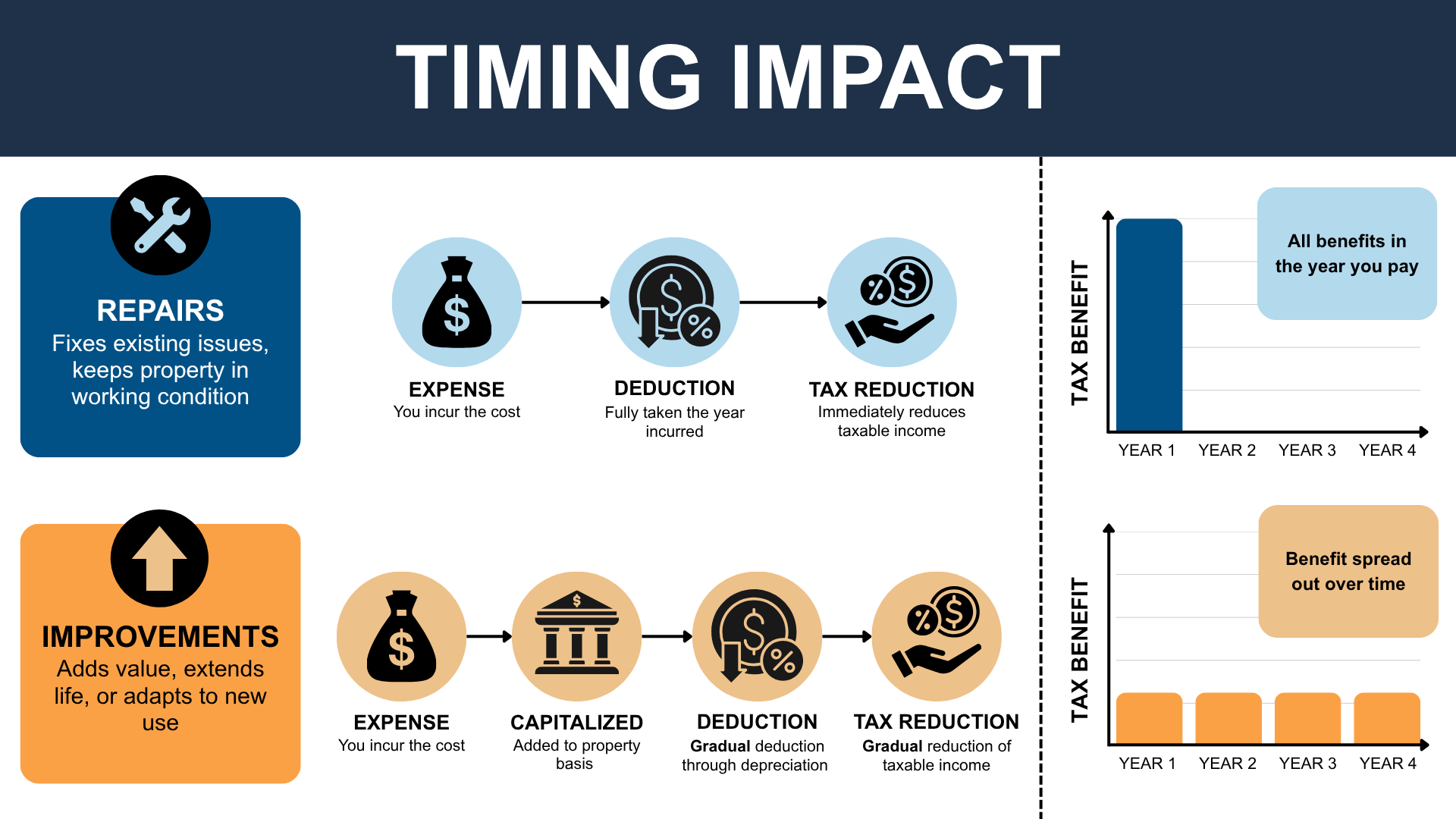

4. Understand Repairs vs Improvements (and Why It Matters)

Beyond standard deductions, there are more advanced opportunities, but they require careful planning. Not all property expenses are treated the same for tax purposes, and misclassifying them can impact your deductions.

Repairs fix existing issues and keep the property in working condition. For example, fixing a leak, repainting, replacing a broken appliance.

Improvements however add value, extend the life of the property, or adapt it to new use. For example, a new roof, HVAC system, or major renovations (think a new kitchen renovation as opposed to just replacing your broken refrigerator)

This distinction is important because repairs are generally fully deductible in the year they are incurred- reducing your taxable income immediately. Improvements however must be capitalized and depreciated over time- spreading the deduction over multiple years.

For vacation rental owners who frequently maintain or upgrade their property, timing and properly categorizing these expenses can make a noticeable difference in your tax outcome in a given year. For example, if your property generates strong rental income this year and you’d like to offset your tax liability, prioritizing necessary repairs before year-end may allow you to take the full deduction immediately.

For vacation rental owners who frequently maintain or upgrade their property, timing and properly categorizing these expenses can make a noticeable difference in your tax outcome in a given year. For example, if your property generates strong rental income this year and you’d like to offset your tax liability, prioritizing necessary repairs before year-end may allow you to take the full deduction immediately.

5. Passive Activity Loss Rules

Rental income is generally considered passive, which means losses may be limited, and you typically can’t use rental losses to offset W-2 income. However, there are two key exceptions that vacation rental owners should understand.

The $25,000 Special Allowance (Long-Term Rentals)

If you actively participate in managing your rental (approving tenants, setting rates, etc.), you may be able to deduct up to $25,000 of rental losses per year against ordinary income

But there are income limits- you receive the full allowance if your income is $100,000 or less. It Phases out between $100,000–$150,000 and is eliminated entirely above $150,000. This is the most common exception, many higher-income vacation rental owners don’t qualify due to the phaseout.

Short-Term Rental (STR) Non-Passive Treatment

Short term rentals may be excluded from these passive activity rules if you meet the ‘material participation’ standard. In order to not be treated as passive, both must apply:

1. Average Guest Stay is 7 Days or Less – This is because the IRS does not consider properties with very short rental periods to be ‘traditional real estate investments.’ Instead, they may be classified as a trade or business. This threshold can be expanded to 30 days or less if you also provide significant services beyond basic maintenance such as daily cleaning, concierge services, meals, or other hotel-like amenities.

2. You Materially Participate – This means you are materially involved in the operation per the IRS’s material participation tests. The most common way to qualify is spending 500+ hours per year on the rental activity or spending 100 hours more than anyone else managing the property. There are other IRS criteria to be met to satisfy the material participation requirements.

Conclusion

Vacation rentals sit in a unique space between personal use and business activity, which is exactly what makes their tax treatment more nuanced than most owners expect. Small details like how many days you rent the property, how often you use it personally, or how you categorize an expense can significantly impact your overall tax outcome.

The key is consistency and awareness. Understanding how your property is classified, keeping accurate records, and applying the rules correctly throughout the year can help you avoid last-minute surprises and position yourself more effectively at tax time.

As demand for short-term rentals continues to grow and reporting requirements become more transparent, taking a proactive approach can help in the long run. Looking for ways to minimize your tax liability this summer? Reach out to CKH Group to book an initial consultation.

The above article only intends to provide general financial information and is based on open-source facts, it is not designed to provide specific advice or recommendations for any individual. It does not give personalized tax, financial, or other business and professional advice. Before taking any form of action, you should consult a financial professional who understands your particular situation. CKH Group will not be held liable for any harm/errors/claims arising from the articles. Whilst every effort has been taken to ensure the accuracy of the contents, we will not be held accountable for any changes that are beyond our control.